AI Invasion · Investigative Analysis · June 2026

AI in Smart Homes 2026:

The Complete, Unfiltered Reality Check

A $31.9-billion industry. 82% household penetration. And most of what you’ve read about it is marketing dressed as journalism. Here’s the full picture — the genuine energy savings, the real privacy cost, the economics that actually work, and the one uncomfortable truth the whole industry keeps dodging.

The Honest Starting Point: What “AI at Home” Actually Means in 2026

Let me be straight with you about something I got wrong. For the better part of 2023 and 2024, I wrote and thought about AI smart homes as if the interesting story was the gadgets — the robot vacuums that could recognize your cat, the fridges that texted grocery lists, the thermostats that “learned” your preferences. I was missing the actual story. The gadgets were never the point. The data architecture was always the point. Once I understood that, everything about this industry looked different.

In 2026, an AI-equipped home doesn’t just run appliances. It runs a continuous, self-updating behavioral model of the people who live inside it. Every time you turn a light on at 6:47 a.m., every time you lower the thermostat before bed, every time your kitchen motion sensor detects someone raiding the fridge at 2 a.m. — that data feeds a system that is, in effect, learning to predict what you want before you want it. That is an extraordinary achievement of engineering. It is also a set of implications most homeowners haven’t thought through.

This piece is an attempt to give you the full picture. Not a product review. Not a “best smart home devices” listicle. A genuine analytical deep-dive into how AI is reshaping the home in 2026 — the energy economics, the security capabilities, the privacy tradeoffs, the market structure, and the hard questions nobody asks in the press release.

When this article uses “AI smart home,” it means residential environments where machine learning, neural networks, or large language model inference is operating at the device, hub, or cloud level to automate, predict, personalize, or optimize home systems. This is distinct from simple rule-based “smart” devices (a timer is not AI; a thermostat that models your behavioral patterns is).

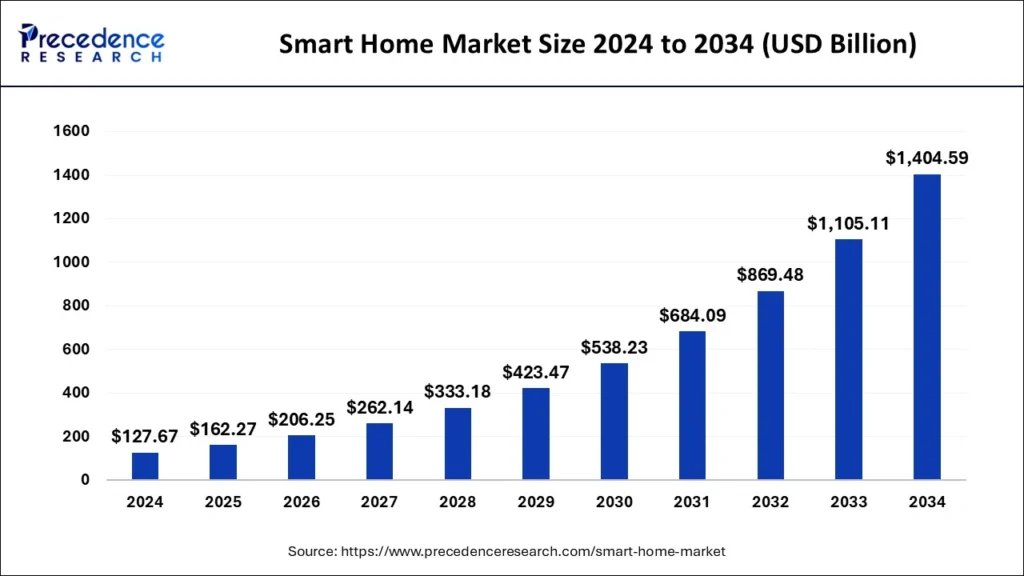

Market Reality: $31.9 Billion and Climbing

Depending on which analyst firm you ask, the global smart home market is “worth” anywhere from $121 billion to $450 billion. This variance isn’t methodology error — it’s scope disagreement. Some figures include all smart devices (anything with an app). Others isolate only AI-inferencing residential systems. For this analysis, the most relevant metric is the specifically AI-in-smart-home segment, pegged by Future Data Stats at $31.9 billion in 2026, expanding to $129.4 billion by 2033 at a compound annual growth rate of 23%. The broader smart home hardware market, per Statista, is tracking toward $175.1 billion in 2026 revenue globally.

What does that growth mean structurally? Three things.

First, AI is becoming non-optional in premium hardware. In 2022, an AI feature was a marketing upsell. In 2026, any smart home device that can’t do some form of local inference — anomaly detection, occupancy prediction, voice pattern recognition — is losing shelf position to one that can. The product category has re-platformized around intelligence.

Second, the revenue split is shifting toward services. Subscription services for cloud storage and AI analytics exceeded $3.2 billion in 2025 alone in the U.S. market. The real economic model for companies like Ring, Nest, and Vivint isn’t device sales — it’s recurring software revenue, which carries 60–80% gross margins compared to 20–35% for hardware.

Third, geographic power is shifting east — fast. China is the single largest national smart home market by revenue in 2026 ($40.2 billion, per Statista), and the Asia Pacific region is on track for the highest CAGR of all regions through 2030. Xiaomi’s ecosystem alone encompasses over 700 million connected devices globally as of early 2026. The Western narrative that AI home technology is an American story — Amazon, Apple, Google — is increasingly out of date.

Sources: Future Data Stats (2026); Fortune Business Insights (2026); Statista Smart Home Market Forecast (2026). Note: regional figures reflect smart home market broadly; AI-specific segment is a subset.

The Energy Equation: Real Savings, Real Costs, Real Math

The claim you’ll see most often in smart home marketing is something like “save up to 30% on your energy bills.” That figure comes from industry-wide modeling and isn’t fabricated — but it’s also not a number most households should expect. Let’s do the actual math.

What the data actually says

According to SQ Magazine’s 2026 analysis of smart home adoption data, 8.4 billion kWh of energy were saved globally in 2025 due to smart home automation — a meaningful aggregate that masks enormous variation at the household level. The specific mechanisms matter enormously:

Smart thermostats with geofencing features save 7–12% more on HVAC costs compared to manual settings. IoT-integrated HVAC systems showed a 12% increase in overall HVAC efficiency in 2025. Smart plugs and switches reduce phantom load (standby power drain) by 15–20%. And 41% of smart home users have set automated schedules for lights, appliances, and HVAC — the cohort that actually captures most of these savings.

Here’s what that means in household terms. The average U.S. household spends approximately $1,500 per year on electricity (EIA data, 2025). HVAC typically represents 40–50% of that — call it $650. A 10% thermostat saving on that portion is $65/year. Add 17.5% phantom-load savings on a $200 annual standby-power bill, and you’re at $35/year additional. Total realistic annual saving: roughly $100–$180 for an average household.

Now cross that against actual hardware costs. A quality AI thermostat (Ecobee, Nest Learning) runs $180–$250. Smart plugs, $40–$80 for a set. A hub, if needed, $80–$150. You’re at $300–$480 in hardware to capture those savings. Payback period: 2–5 years. That’s a reasonable but not remarkable ROI — and it only holds if you don’t count the ongoing cloud subscription costs, which for Ring Protect Plus run $20/month or $200/year.

Author calculations based on EIA average household energy data (2025), SQ Magazine smart home statistics (2026), and retail hardware pricing. Individual results vary significantly by home size, utility rates, and usage patterns.

If you add a $200/year cloud subscription to a security-enabled AI home setup, your “energy savings” from smart home technology are entirely consumed paying for the software layer. The net financial benefit, in many average-use scenarios, is near-zero for the first three to five years — until hardware is fully amortized and subscriptions are either dropped or replaced by local-processing alternatives.

Where the math genuinely works

The cases where AI energy management delivers clearly positive ROI: households with above-average HVAC costs (hot/cold climates, larger homes), homes with solar panels where AI can optimize self-consumption vs. grid export, and multi-dwelling units where aggregated savings across tenants cover infrastructure costs more efficiently. In California, where electricity averages $0.28/kWh versus the national average of $0.16/kWh, the savings multiply proportionally — and the payback period can shrink to 18 months.

AI-Powered Security: Remarkable — and Quietly Frightening

This is where AI earns its keep most visibly. The security and access control segment held over 29% of the smart home market in 2024 and continues to lead by revenue — because AI genuinely transforms what home security can do.

Traditional motion-triggered cameras generated so many false alarms (passing cars, blowing leaves, neighborhood cats) that most homeowners disabled the notifications within a week. AI-powered cameras changed this by learning to distinguish between human presence, animal movement, and environmental motion with accuracy rates that have improved dramatically. Amazon’s Ring lineup, Google’s Nest Cam, and Arlo’s systems with Origin AI’s TruShield technology now use neural networks running either locally or in the cloud to verify human presence before triggering alerts. The practical impact is substantial: 52% of homeowners report feeling significantly safer with smart home security systems in place, according to 2025 data from SQ Magazine’s smart home tracking survey.

The January 2026 launch of Amazon’s Alexa Predictive Care, integrated into the Echo Show 15, added a genuinely new capability: behavioral AI that can detect anomalies in elderly residents’ daily routines — unusual stillness, changes in movement patterns, potential fall indicators — and alert caregivers. This represents AI crossing a meaningful threshold from convenience to care infrastructure.

The shadow side

Here’s what the marketing material doesn’t tell you: Bitdefender’s threat intelligence team documented in late 2025 that smart plugs, smart TVs, and consumer electronics were among the most frequently targeted device categories in global attacks on home networks. A compromised smart plug is not just a smart plug problem — it becomes a lateral entry point into every other device on the same network segment. Every phone, laptop, and financial account your browser is logged into.

The 2022 iRobot Roomba incident — where photos captured by a robot vacuum during AI training ended up on Facebook — wasn’t an isolated glitch. It was a demonstration of how data governance in AI home devices can fail at every level: collection, storage, transmission, and vendor control. When you introduce any camera-equipped, cloud-connected AI device into your home, you are, by definition, operating within the data governance decisions of a company that may be acquired, may change its terms of service, or may be breached.

Constructed from Bitdefender threat intelligence documentation (late 2025) and IMARC/Grand View Research security segment analysis. Positions are qualitative assessments, not precise numerical scores.

Matter Protocol in 2026: Finally Working — Mostly

Two years ago, Matter was a promise. Today it’s a functioning standard with serious caveats.

The Connectivity Standards Alliance reports that over 750 Matter-certified products were on market as of mid-2026, with the standard now running in 38% of Home Assistant instances and supported across all four major ecosystems: Apple Home, Google Home, Amazon Alexa, and Samsung SmartThings. Matter 1.6, released in June 2026, is the current specification. The immediately preceding Matter 1.5 and 1.5.1 updates (November 2025 and March 2026 respectively) added camera support, HEIC snapshot handling, and significant improvements to multi-stream video delivery — the practical features that made Matter actually useful for security systems.

The promise of Matter — buy any certified device, have it work with any ecosystem — is substantially closer to reality in 2026 than it was in 2023. Smart locks from Yale and Schlage, thermostats from Ecobee and Honeywell Home, and lighting from Nanoleaf and Philips Hue now work seamlessly across platforms. This is genuinely significant. The walled-garden era of smart home technology — where buying a Nest thermostat meant committing to Google’s ecosystem — is functionally over for new device categories.

The honest caveats

But here’s what the enthusiast press underplays: ecosystem implementation consistency remains a real problem. As matter-smarthome.de documented in January 2026, while Samsung SmartThings moved rapidly to adopt Matter 1.5 features, Google Home remained stuck on version 1.2 for certain device categories at the same time — meaning an Ikea Bilresa remote control works in SmartThings but fails in Google Home, despite both being “Matter compatible.”

The label “Matter certified” on a box doesn’t mean “works identically across all platforms.” It means “passes the CSA’s interoperability test suite at the time of certification.” Platform-specific feature limitations, firmware update timing differences, and ecosystem-level implementation choices mean that advanced features — particularly energy management and camera functionalities from Matter 1.5 — can be available in one ecosystem months before another.

“The seeds have been sown and Matter is spreading as a grassroots movement: decentralized, without any set direction. The standard is growing from the bottom up into the smart home sector.”

— matter-smarthome.de analysis, January 2026

| Feature Category | Apple Home | Google Home | Amazon Alexa | SmartThings | Home Assistant |

|---|---|---|---|---|---|

| Basic lighting & switches | ✓ Full | ✓ Full | ✓ Full | ✓ Full | ✓ Full |

| Smart locks & access | ✓ Full | ✓ Full | ✓ Full | ✓ Full | ✓ Full |

| Thermostats / climate | ✓ Full | ✓ Full | ✓ Full | ✓ Full | ✓ Full |

| Cameras / doorbells (M 1.5) | ✓ Full | ⚡ Partial | ✓ Full | ✓ Full | ✓ 1.5.1 |

| Energy management (M 1.3+) | ⚡ Limited | ✗ Lagging | ⚡ Partial | ✓ Active | ✓ Full |

| Generic switches (M 1.0) | ✓ Full | ✗ Not exposed | ✓ Full | ✓ Full | ✓ Full |

Based on matter-smarthome.de review (Jan 2026), Home Assistant blog (Jun 2026), programming-helper.com analysis (Apr 2026), and Data Wire Solutions (Jun 2026). Status subject to change with platform updates.

The Privacy Bargain You Haven’t Fully Priced In

I want to be careful here because this section could easily tip into paranoia — which is just as misleading as false reassurance. The privacy risks of AI smart homes are real, specific, and manageable. They are not a reason not to use smart home technology. They are a reason to understand what you’re actually agreeing to.

Cloud-connected smart home devices send usage data, voice recordings, and camera footage to company servers where it can be retained, shared with third parties, or exposed in a breach. This isn’t a conspiracy theory. Bloomberg documented in 2019 that both Amazon and Google employed contractors to listen to user voice assistant recordings — including clearly private conversations — without user notification. Both companies now offer opt-outs. According to a 2026 privacy analysis by PromptQuorum, almost nobody uses those opt-outs because almost nobody knows they exist.

The emerging structural response to this is the edge-AI architecture — processing on-device rather than in the cloud — which we’ll cover in Section 9. But it’s worth noting that the privacy landscape of AI homes in 2026 is at an inflection point. As Gadgonic’s February 2026 analysis noted: “Regulations are tightening around data collection, pushing more on-device processing and transparent AI. Expect widespread adoption of local AI models, better Matter encryption standards, and user-controlled privacy dashboards.”

The privacy-as-product-differentiator move is also gaining commercial momentum. Josh.ai, demonstrated at ISE 2026 by CEO Alex Capecelatro, has built its entire luxury smart home platform around local processing and reduced cloud dependency — and is finding a willing market among high-net-worth buyers who understand what they’re trading.

Security researchers have demonstrated that three seconds of audio is sufficient to produce a convincing AI voice clone. Every audio clip stored on Amazon’s, Google’s, or Apple’s servers is, in principle, training data that survives a data breach with permanent consequences. Unlike a password, a voice cannot be changed after it’s compromised. This is not theoretical: major tech company breaches are a historical pattern, not a hypothetical.

The HAIL Framework: How to Grade Any AI Home Investment

I developed the HAIL Framework after spending too much time watching smart home buyers make decisions based on marketing claims rather than a structured evaluation of what they were actually getting. It has four dimensions, each of which should be scored before any AI home purchase:

The HAIL Framework for AI Home Investment Evaluation

Rate each dimension 1–5. Any purchase scoring below 12/20 total warrants serious reconsideration. Any dimension scoring 1 is a potential dealbreaker depending on your priorities.

Does the device have a credible multi-year support commitment? Is the manufacturer financially stable? Will firmware updates continue if the company is acquired? (Ring under Amazon: relatively stable. Smaller startups: less certain.)

Where does inference run — locally or in the cloud? Local-first means it works without internet, costs no subscription, and your data stays home. Cloud-first means ongoing costs and privacy exposure. Hybrid is the current middle ground.

Is this device Matter-certified? If not, what’s the exit strategy? Can you migrate to a different ecosystem without replacing the hardware? The best devices today have answers to all three questions.

What is the total cost of ownership over five years? Hardware + subscriptions + installation + energy. What are the measurable savings or value additions? What’s the payback period at realistic (not marketing) savings estimates?

Author’s qualitative HAIL framework scores, based on published product specifications, subscription terms, Matter certification status, and lifecycle cost modeling (2026).

Unit Economics of the AI Home: What You Spend vs. What You Get

Let’s build a full household model. This is the analysis I wish someone had given me before I started buying devices.

Scenario: A 2,000 sq ft single-family home, fully AI-equipped (U.S., 2026)

Author modeling based on: retail hardware pricing (2026), SQ Magazine subscription cost data, EIA residential energy averages, and realistic (not marketing-claim) efficiency savings estimates.

The key insight from this model: the premium edge-local setup has the highest upfront cost but the best long-term privacy profile and no subscription exposure. The entry-level cloud-dependent setup looks cheapest but is optimized for vendor revenue, not homeowner value. The mid-tier hybrid is where most households will reasonably land in 2026.

The hidden value that doesn’t appear in cost models

Property value impact is real and increasingly measurable. A 2025 National Association of Realtors survey found that smart home features increased perceived property value by 3–5% in competitive markets. On a $400,000 home, that’s $12,000–$20,000 in value creation — which makes even the premium scenario’s $3,800 net cost look like an excellent investment. This effect is most pronounced in markets where competing listings standardly feature AI home systems.

The Edge-vs-Cloud War and Why It Matters to You

The most significant technical divide in AI homes right now isn’t about devices — it’s about where intelligence lives. The architectural decision between edge processing (AI runs on-device or on a local hub) and cloud processing (AI runs on vendor servers) affects privacy, latency, reliability, subscription costs, and long-term ownership in ways most consumers never think about when they open a box.

Samsung’s SmartThings Edge AI Hub (launched November 2025) processes data locally for real-time anomaly detection in energy usage and appliance faults — no cloud round-trip required. Apple’s HomePod with Siri LLM integration (August 2025) added adaptive scene generation that learns routines in 24 hours while keeping most processing on-device. These are meaningful architectural commitments, not just marketing language.

The open-source community has been living this reality for years. Home Assistant, running on a Raspberry Pi or local mini-PC, now enables genuinely capable local AI inference through integrations with tools like Ollama (for local LLM functionality) and local-only computer vision models. You get smart home functionality without a single byte of personal data leaving your house. The tradeoff is setup complexity — this isn’t plug-and-play for most users, though the community has worked hard to reduce that gap.

Framework based on Gadgonic AI Privacy Smart Home review (Feb 2026), PromptQuorum local smart home analysis (Jun 2026), and Samsung/Apple product specification documentation (2025–2026).

The Unpopular Take: AI Homes Are Still a Luxury Product Pretending Not to Be

I said at the start I’d include an uncomfortable truth. Here it is.

The smart home industry is excellent at performing mass-market accessibility while remaining structurally oriented toward affluent early adopters. The average annual smart home spending per U.S. household is $2,500. The median U.S. household income is approximately $74,500. We’re talking about 3.4% of gross income allocated to home technology — a figure that concentrates sharply in higher income brackets. The 82.1% household penetration statistic from Statista measures “smart home devices” broadly, including any internet-connected device. A $35 smart plug counts. A $25 smart bulb counts. The meaningful AI-reasoning, behavioral-learning, full-stack smart home that generates actual ROI? That’s a different population.

Retrofit installation is now the fastest-growing smart home market segment globally — which sounds like democratization but largely means that homeowners with existing, owned properties are adding smart features. Renters, who represent a growing share of households in most major cities, are systematically excluded from most meaningful smart home deployments because landlords have no economic incentive to invest in improvements that increase their tenants’ quality of life without raising rent.

The energy efficiency gains that AI homes deliver are most powerful for the households that consume the most energy — large homes with central HVAC, multiple occupants, complex usage patterns. A 10% saving on a $300/month energy bill is $360/year. A 10% saving on a $60/month energy bill is $72/year. The households most burdened by energy costs tend to have fewer smart home resources to deploy and smaller absolute savings even when they do. I don’t think this means smart home technology is bad. I think it means the industry should be honest about who the primary beneficiary actually is — which is not “everyone.”

“AI homes improve energy efficiency by 30% — on paper. In practice, that figure applies to an ideal deployment at above-average scale. For the median household, realistic savings are closer to 8–12%. Both numbers are real. They describe different populations.”

— AI Invasion Research analysis, 2026

What 2027–2030 Actually Looks Like

I’m deliberately cautious about future projections because technology forecasting has a well-documented track record of being wrong in interesting ways. But some dynamics are structurally legible from where we are now.

The LLM integration wave is just beginning

Apple’s HomePod Siri LLM integration in August 2025 was the proof-of-concept moment: a large language model running meaningfully in a home context, interpreting natural-language commands of arbitrary complexity rather than fixed-pattern triggers. “Turn off the kitchen lights” is a rule. “Set the house up the way it is on a normal Sunday morning before we go to the farmers market” is LLM territory. The shift from rule-based to language-based home control will make AI home systems dramatically more useful to non-technical users — and will expand the addressable market as a result.

Grid integration as the next major vertical

Matter 1.5’s additions around energy management devices — solar panels, batteries, heat pumps, smart meters — signal the next major expansion: AI homes that participate intelligently in the electricity grid as distributed flexibility assets. A home with a battery, solar panels, an EV charger, and AI-managed HVAC can function as a demand-response resource that earns revenue from utilities during peak demand. This is not science fiction — it’s already commercially available through programs like Sunrun’s Virtual Power Plant in California. The economics will become compelling at scale when AI can automate the optimization without requiring homeowner attention.

The regulatory inflection

The EU’s regulatory focus on data localization will accelerate the edge-AI trend in European markets. California’s SB 253, requiring large companies to disclose Scope 1–3 emissions starting in 2026, will push IoT device manufacturers toward energy transparency. The convergence of privacy regulation (pushing local processing) and emissions regulation (pushing energy efficiency measurement) will, counterintuitively, make AI homes better — by forcing the industry to build systems that perform without continuous cloud dependency.

Constructed from: Statista Smart Home 2029 penetration projections; Future Data Stats 2033 market sizing; EU regulatory timeline (AI Act, Energy Efficiency Directive); author’s structural analysis.

Conclusion: How to Act on This

If you’ve read this far, you probably want more than analysis — you want a decision framework. Here’s mine, in plain language.

If you’re starting from scratch in 2026: Build Matter-native from day one. Don’t buy anything that isn’t Matter-certified or on the roadmap to be. Your ecosystem choice (Apple, Google, Amazon, or open Home Assistant) should be based on which voice assistant you already use and trust — they’re converging fast enough that the ecosystem lock-in of 2022 is now much weaker. Start with the devices that deliver measurable ROI: a smart thermostat, smart plugs on high-draw appliances, and a local hub if you’re technically comfortable.

If you already have smart home devices but they’re fragmented: You don’t need to rip and replace everything at once. The Matter bridge architecture means many older devices can participate in a Matter network through translation devices. Prioritize replacing any cloud-dependent security cameras with local-processing alternatives if privacy matters to you — this is the single highest-leverage privacy improvement you can make.

If you’re evaluating AI home technology for a professional context (developer, builder, property manager): The ROI case is genuinely strong at scale. Multi-unit residential buildings with centralized AI energy management can achieve 15–20% energy savings at the portfolio level — those numbers hold up because the scale makes the overhead costs negligible. The business case in new construction is particularly clear because Matter-compatible hardware doesn’t meaningfully increase construction cost but commands a meaningful premium at sale or rental.

The honest bottom line: AI in smart homes is real, working, and delivering genuine value in 2026 — but the gap between the marketing narrative and the lived reality is still wider than it should be. The energy savings are real but smaller than claimed for most households. The security capabilities are genuinely impressive but introduce new attack surfaces. The privacy tradeoffs are real and underpriced by most buyers. And the interoperability story, while much better than it was two years ago, is not yet as clean as the industry would have you believe.

That’s not a reason to stay out. It’s a reason to go in with your eyes open.

For the primary research underlying this analysis: Future Data Stats AI Smart Home Market (2026) · Statista Smart Home Worldwide Forecast · Matter & Thread Explained 2026 · Home Assistant Matter Server 9.0 (Jun 2026) · SQ Magazine Smart Home Statistics 2026 · Springer AI & Society: Privacy in the Smart Home (2025)

For deeper context on the AI dimension: AI Invasion covers the intersection of artificial intelligence and everyday life across consumer, professional, and societal contexts. Related reading on AI home robotics, LLM integration in consumer devices, and the data-rights landscape for AI-connected appliances.